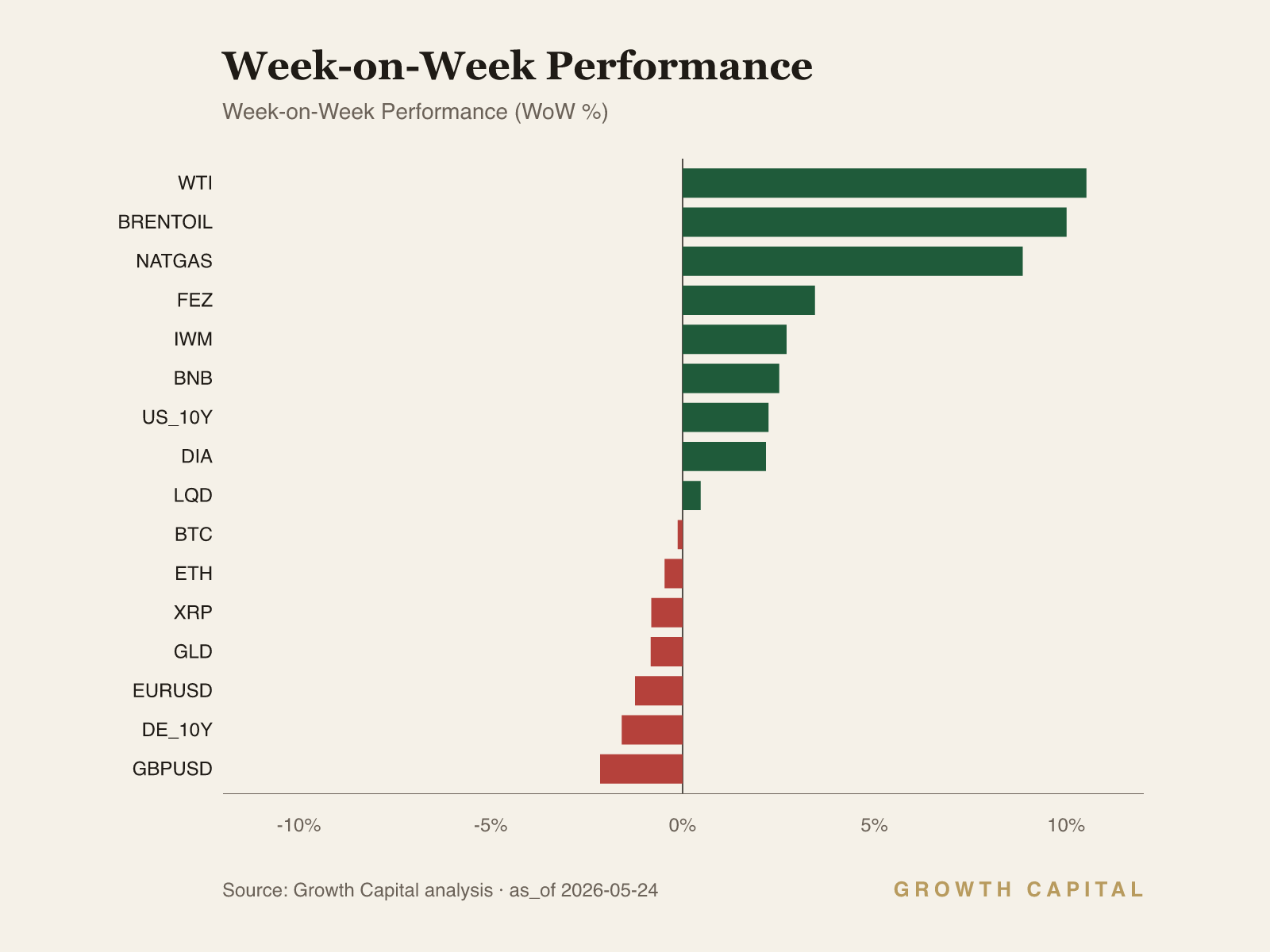

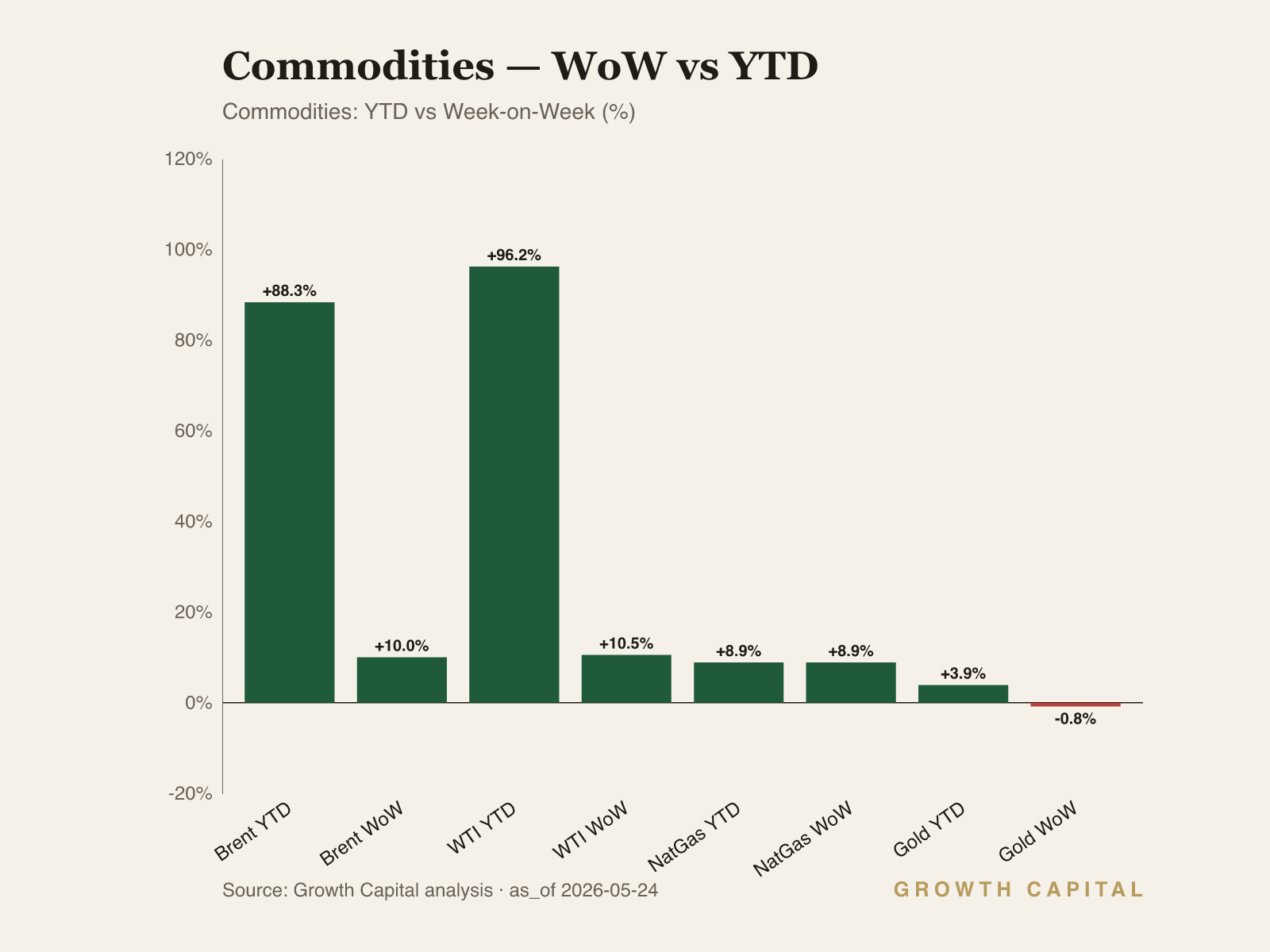

Crude's war premium reshapes the policy calculus. Brent surged +10.0% WoW to $116.73/bbl, its highest level since the Hormuz closure began, while FOMC minutes revealed a growing faction prepared to lay groundwork for rate hikes if inflation stays elevated.

Yields break higher on a divided Fed. The 10Y Treasury yield rose +2.2% WoW to 4.57%, approaching its 52-week high of 4.67%, as the April minutes exposed a four-way dissent split and new Chair Warsh inherits the most fractured committee since 1992.

Equities grind higher on narrow leadership, ignoring the rates signal. SPY gained +0.9% WoW to $745.64, within 0.3% of its all-time high, but the rally was concentrated in energy (+7.0%) and tech (+1.2%) while consumer discretionary fell -3.0%, a breadth divergence that is inconsistent with a durable risk-on regime.

Our positioning: Crude's war premium is rewriting the Fed's reaction function; we are underweight duration and overweight energy.

A hawkish hold with hike optionality is the new baseline as energy costs rewrite the inflation path

We label the current regime a stagflation lean with hike optionality. The April FOMC minutes, released this week, showed an 8-4 vote to hold the federal funds rate at 3.50-3.75%, the widest dissent since 1992. Three regional presidents objected to easing-bias language, while a growing subset of the committee favoured laying groundwork for a rate hike if inflation remains above target. Kevin Warsh was sworn in as the 17th Fed chair on 22 May, inheriting a committee whose median member has shifted from "patient hold" to "conditional tightening." Brent crude at $116.73/bbl, up +10.0% WoW and +88.3% YTD, is the proximate cause: the Strait of Hormuz disruption has shut in roughly 10.5 million barrels per day of Middle East production according to the EIA's May STEO, and the pass-through into headline CPI is only beginning. With the unemployment rate at 4.3% and GDP still running at +2.0% annualised, the Fed faces an energy-driven inflation impulse layered onto an economy that is not yet cooling enough to justify patience.

The 10Y Treasury yield closed at 4.57%, up +2.2% WoW and +9.1% YTD, now sitting just 10 basis points below its 52-week high of 4.67%. The 2Y yield rose +2.0% WoW to 4.08%, pushing the 10Y-2Y spread to +49bp (the snapshot reads 43bp as of 22 May; the Friday close implies further steepening). The mechanism is direct: crude at $116.73 feeds into transport, petrochemical, and food-processing costs with a lag of roughly two to four months, lifting breakeven inflation expectations. Governor Waller, speaking in Frankfurt on 22 May, flagged energy-price disruptions as a primary concern for the inflation outlook. Higher breakevens compress the real-rate cushion the Fed had built during the 2024-25 easing cycle, which means the committee's revealed preference for a conditional hike is not posturing but a rational response to a supply shock that monetary policy cannot resolve but must prevent from embedding in wage expectations. The pass-through from Brent to US CPI has historically run at roughly 3-5 cents per gallon per dollar of crude, and with WTI at $112.25 (up +10.5% WoW, +96.2% YTD), gasoline prices are already feeding consumer sentiment deterioration. We are underweight duration (UW on US_10Y) with a 3-6 month horizon, accepting the carry cost of being short bonds in a rising-yield environment. The trade-off is explicit: if the Hormuz situation resolves faster than expected (Trump announced a deal framework on 24 May), the war premium in crude could collapse $20-30/bbl, pulling yields back toward 4.20-4.30%. We would revisit our UW duration stance if the 10Y yield falls below 4.30% on a weekly close, which would signal the market is pricing a credible de-escalation rather than a headline bounce.

Equities present a surface contradiction to the rates signal that we resolve in favour of caution. SPY closed at $745.64, up +0.9% WoW and +9.1% YTD, sitting 0.3% below its all-time high of $748.17. QQQ gained +1.2% WoW to $717.54, +17.0% YTD, also near its 52-week peak. But the rally's internals are fragile. Energy led the week at +7.0%, a mechanical beneficiary of the crude surge, while consumer discretionary fell -3.0%, reflecting the margin squeeze that $112 WTI imposes on household budgets. DIA's +2.2% WoW gain to $506.12 (a new all-time high) was driven by healthcare (+3.4%) and industrials, not broad participation. IWM's +2.7% WoW move to $285.12 looks constructive on the surface, but small-cap earnings are more exposed to input-cost inflation than mega-cap tech, and the Russell 2000's +14.6% YTD gain has been built on multiple expansion rather than earnings delivery. The equity tape confirms the energy-driven rotation but contradicts the P1 regime read on duration: if the Fed is moving toward hike readiness, the forward earnings discount rate rises, and the S&P 500's current implied equity risk premium (compressed by the rally to near-cycle lows) offers insufficient compensation. We are neutral on SPY, not underweight, because the energy sector's earnings tailwind and still-positive GDP growth provide a floor, but we would shift to UW if the 10Y yield breaches 4.67% on a weekly close, which would signal the bond market is pricing a hike cycle rather than a single adjustment.

The dollar's behaviour this week confirms the hawkish-hold thesis. DXY rose +1.1% WoW to 119.28, a six-week high, supported by the manufacturing PMI jumping to 55.3 (fastest in four years) and initial jobless claims falling to 209,000. EUR/USD fell -1.2% WoW to 1.1627 as the German 10Y Bund yield actually declined -1.6% WoW to 3.10%, creating a widening transatlantic rate differential. USD/JPY climbed +1.3% WoW to 158.69, approaching the 160.23 level that triggered intervention concerns in prior cycles. The dollar's strength is a tax on EM and commodity importers, but for US-domiciled allocators it reinforces the case for staying overweight domestic assets. GLD fell -0.8% WoW to $413.82, a second consecutive weekly decline that reflects gold's sensitivity to rising real yields rather than any diminution of geopolitical risk. We view gold as neutral at current levels: the war premium supports a floor, but the real-yield headwind caps upside until the Fed's direction clarifies.

Source: GrowthCapital analysis; FRED, EIA May 2026 STEO, FOMC April 2026 minutes.

Commodities

Brent crude closed at $116.73/bbl, up +10.0% WoW and +88.3% YTD, while WTI surged +10.5% WoW to $112.25, breaching its prior 52-week high of $114.58 intraweek. The EIA's May Short-Term Energy Outlook estimates roughly 10.5 million barrels per day of Middle East production shut in through late May, with a gradual Hormuz reopening assumed but not yet confirmed. The late-week announcement of a Trump-Iran deal framework to reopen the Strait triggered a sharp sell-off on Hyperliquid perpetuals, pushing WTI toward the high-$80s in after-hours trading, but the spot close remained elevated. This divergence between derivatives repricing and physical settlement is the key tension: if the deal holds, the war premium (which we estimate at $25-30/bbl based on pre-conflict Brent levels near $62) unwinds rapidly, but OPEC+ spare capacity is thin and any re-escalation would push Brent toward its 52-week high of $138.21. Natural gas rose +8.9% WoW to $3.07/MMBtu, a modest move relative to crude but consistent with seasonal demand and LNG export substitution for lost Middle East supply. We are overweight Brent crude on a 1-3 month horizon, with the view that the Hormuz premium persists until physical flows normalise, not merely until a deal is announced. The falsifier is a sustained WTI close below $95, which would signal the market believes the deal is durable and spare capacity is being released. GLD at $413.82 (-0.8% WoW) is caught between geopolitical bid and real-yield drag; we hold neutral, awaiting clarity on the Fed's next move.

Fixed Income

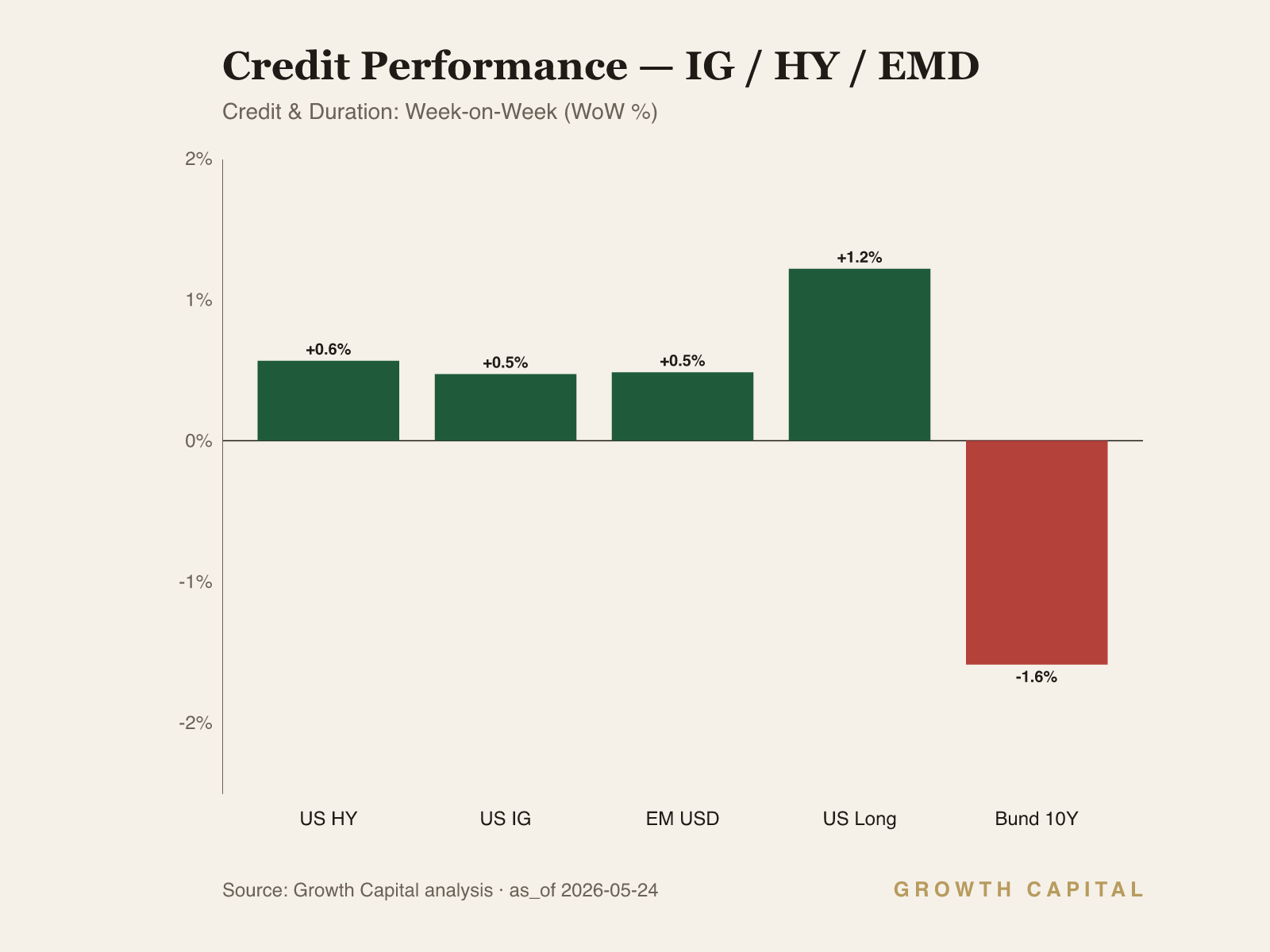

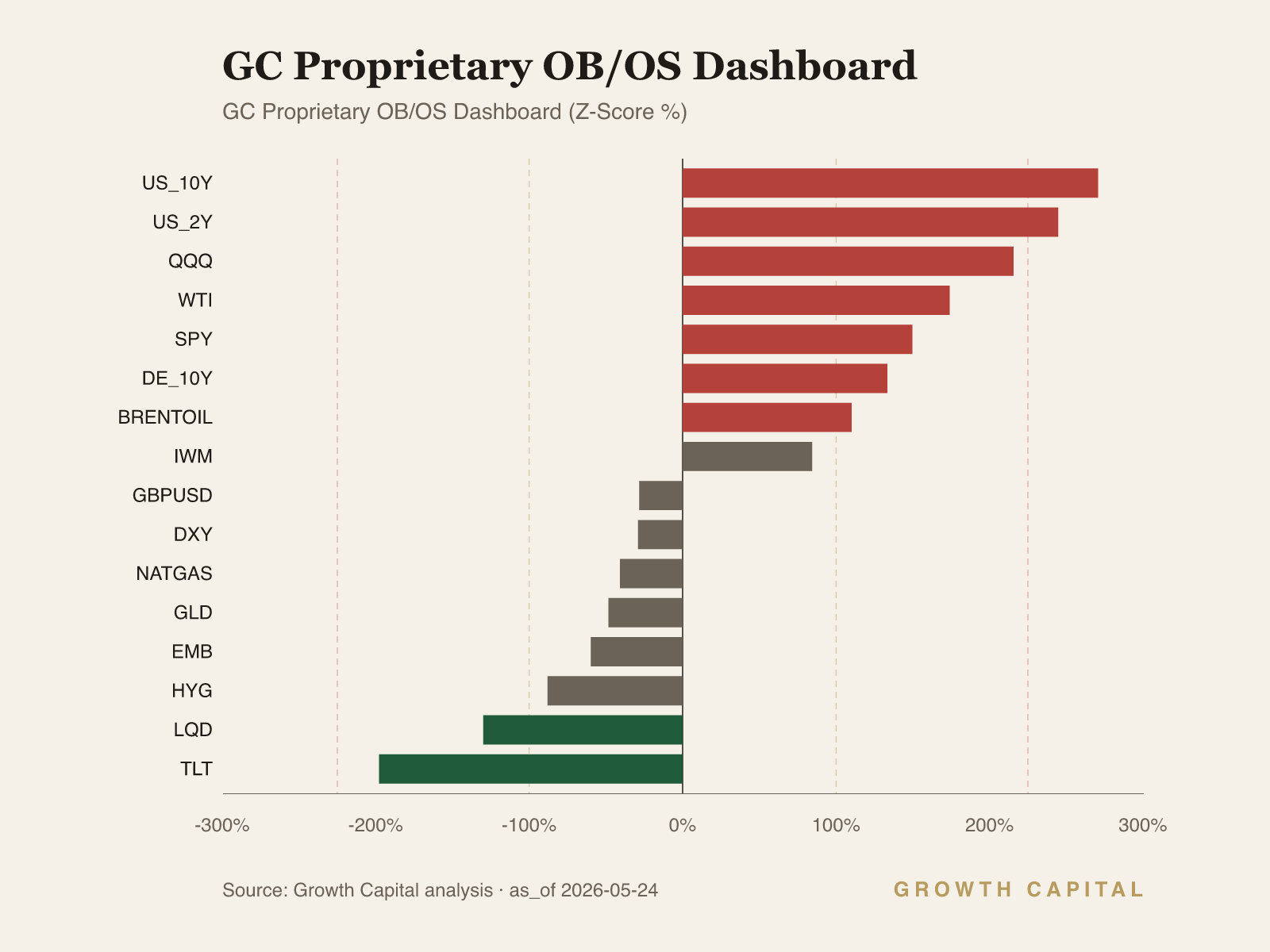

The 10Y Treasury yield at 4.57% is now overbought on a technical basis and sits 10bp below its 52-week high of 4.67%, a level that would represent the tightest financial conditions since the pre-easing cycle. The 2Y yield at 4.08% (+2.0% WoW, +17.6% YTD) has repriced more aggressively than the long end in percentage terms, reflecting the front-end's sensitivity to the FOMC's revealed hike optionality. The 10Y-2Y spread at 43bp (as of 22 May) remains positive, consistent with a bear-steepening regime where term premium is rising on fiscal and inflation uncertainty rather than recession expectations. TLT at $84.68 (+1.2% WoW) bounced modestly from its 52-week low of $83.02, but remains -2.7% YTD, and the slightly oversold reading suggests limited near-term downside from here absent a fresh catalyst. LQD at $108.37 (+0.5% WoW) and HYG at $79.91 (+0.6% WoW) both recovered marginally, but investment-grade credit is -1.6% YTD and high-yield -0.9% YTD, underperforming duration-matched Treasuries. This spread compression in credit, with HYG trading near the middle of its 52-week range ($78.72-$81.32), tells us the market is not yet pricing recession risk from the oil shock, only the rates adjustment. EMB at $95.17 (+0.5% WoW) is similarly range-bound. We are underweight the 10Y, expecting yields to test 4.67% within the next two to four weeks as the crude-to-CPI pass-through materialises. A weekly close below 4.30% on the 10Y would flip us to neutral, signalling the market has priced a credible Hormuz resolution.

Equities

SPY at $745.64 is slightly overbought and 0.3% from its all-time high, a positioning that looks precarious given the rates backdrop. The week's +0.9% gain was driven by energy and healthcare, not the broad-based tech leadership that characterised the Q1 rally. QQQ's +1.2% WoW gain to $717.54 was supported by Nvidia's guidance and AI infrastructure spending (Nokia +10.6% on AI-related projects, ASML +4.7%), but the Nasdaq's +17.0% YTD return is increasingly concentrated in a handful of names. DIA's +2.2% WoW move to $506.12 set a new all-time high, led by defensive sectors. IWM's +2.7% WoW to $285.12 was the strongest US index move, but small caps face the most direct margin pressure from $112 WTI through higher transport and input costs. In Europe, FEZ gained +3.4% WoW to $67.19, with the STOXX 50 reaching 6,025 on tech and bank strength, though the Bund yield's -1.6% WoW decline to 3.10% provided a tailwind that US equities did not enjoy. EWJ at $91.61 (+0.6% WoW) continues its +12.6% YTD run, supported by yen weakness (USD/JPY at 158.69) and AI-related flows into SoftBank. We are neutral on SPY: the energy earnings tailwind and positive GDP offset the duration headwind, but the risk-reward is asymmetric to the downside if yields breach 4.67%. We would move to underweight on a 10Y close above 4.67% or an S&P 500 weekly decline exceeding 3%.

Forex

DXY at 119.28 (+1.1% WoW) reached a six-week high, driven by the widening US-Europe rate differential and safe-haven demand amid Hormuz uncertainty. The dollar's YTD return is -0.3%, meaning the weekly move has nearly erased the year's prior weakness. EUR/USD fell -1.2% WoW to 1.1627 as the ECB's policy stance remains more dovish than the Fed's newly hawkish tilt; the German Bund yield's decline to 3.10% while the US 10Y rose to 4.57% creates a 147bp transatlantic spread that favours dollar longs. GBP/USD dropped -2.2% WoW to 1.3332, the sharpest weekly decline among G10 pairs, reflecting UK exposure to energy-import inflation and a Bank of England that lacks the Fed's hawkish pivot. USD/JPY at 158.69 (+1.3% WoW) is approaching the 160.23 level that historically triggers Japanese intervention rhetoric; the yen's weakness is a direct function of the BOJ's yield-curve-control persistence while US real yields climb above 3.5%. USD/CHF rose +1.2% WoW to 0.7868, consistent with the broad dollar bid. We are neutral on EUR/USD at current levels: the rate differential supports further dollar strength, but the DXY is mid-range within its 52-week band (117.44-123.07), and a Hormuz deal that collapses crude would reduce the Fed's hike urgency, weakening the dollar. We would turn bearish on the dollar if DXY falls below 117.44 on a weekly close.

GC Views

| Asset | View | Rationale |

|---|---|---|

| US_10Y | UW | Crude-to-CPI pass-through and Fed hike optionality push yields toward 4.67% 52wH; UW duration on 3-6 month horizon. |

| SPY | N | Energy earnings tailwind offsets duration headwind at +9.1% YTD; narrow breadth caps conviction for OW. |

| BRENTOIL | OW | Hormuz premium persists until physical flows normalise; +88.3% YTD with 10.5M b/d shut-in per EIA STEO. |

| GLD | N | Geopolitical floor vs real-yield drag at 3.5%+ creates a range-bound setup; -0.8% WoW, +3.9% YTD. |

| BTC | N | Smart money net short on Hyperliquid; -13.6% YTD with 57.3% dominance signals defensive rotation. |

| EURUSD | N | 147bp US-DE spread supports dollar but DXY mid-range in 52w band; await Hormuz resolution clarity. |

| WTI | OW | War premium of $25-30/bbl persists; +96.2% YTD, breached prior 52wH of $114.58 intraweek. |

| QQQ | N | +17.0% YTD concentrated in AI names; overbought near 52wH of $719.79, vulnerable to rates repricing. |

| DIA | N | New ATH at $506.12 on defensive rotation; +4.7% YTD lags SPY, limited upside catalyst. |

| IWM | N | +14.6% YTD on multiple expansion; small-cap margins most exposed to $112 WTI input costs. |

| US_2Y | UW | Front-end repricing +17.6% YTD on hike optionality; 2Y at 4.08% near 52wH of 4.13%. |

| TLT | UW | Slightly oversold at $84.68 but -2.7% YTD; bear-steepening regime favours short duration. |

| DXY | N | Six-week high at 119.28 on rate differential; mid-range in 52w band, Hormuz deal is the swing factor. |

On-Chain Pulse

The on-chain picture across major digital assets this week shows broad risk-off positioning on Hyperliquid perpetuals. Smart money and whales are collectively net short on BTC, ETH, and XRP, while total crypto market capitalisation sits at $2.68 trillion with BTC dominance at 57.3%. The 24-hour volume of $106.2 billion is adequate but not indicative of capitulation or euphoria. The pattern is consistent with a macro environment where rising real yields and dollar strength compress the appeal of zero-coupon risk assets.

Bitcoin traded at $76,687, down -0.1% WoW and -13.6% YTD, with Hyperliquid open interest at $2.1 billion and 7-day volume of $15.4 billion. Smart traders are net short $27.3 million (longs $36.3 million versus shorts $63.6 million), a decisive bearish lean from the cohort with the strongest historical hit rate. Whales are net short $45.4 million, with longs of $122.5 million against shorts of $167.8 million, representing a roughly 58% short exposure ratio that exceeds the smart-trader skew. On the spot side, WBTC exchange flows showed $13.9 million in net inflows over seven days, a bearish signal consistent with distribution rather than accumulation. The funding rate is -0.21% annualised, mildly negative but not at levels that typically trigger short squeezes. Notable positions include Selini Capital with $21.4 million aggregate long (entry around $76,500) and Galaxy Digital with a $4.4 million long at $76,797, both swimming against the aggregate flow. We hold BTC at neutral: the smart-money short lean is a headwind, but BTC's 57.3% dominance and relative outperformance versus altcoins (-13.6% YTD vs ETH's -30.1%) suggest it remains the defensive allocation within crypto. A move above $85,000 with positive funding would challenge this read.

Ethereum at $2,100.98 is down -0.5% WoW and -30.1% YTD, the weakest major by year-to-date performance. On Hyperliquid, the derivatives picture mirrors BTC's bearish tilt but with less granular cohort data available in this week's intel. The broader pattern of smart-money and whale net shorts across the complex applies to ETH, and the -3.57% seven-day performance on the derivatives mark ($2,101.50) slightly exceeds the spot decline, suggesting perps are leading the move lower. ETH's underperformance relative to BTC (a -16.4 percentage point YTD gap) reflects the market's preference for the higher-dominance, more liquid asset during risk-off regimes. Funding rates across the ETH complex remain negative, consistent with the short bias. We are underweight ETH: the combination of smart-money shorts, negative funding, and severe YTD underperformance suggests the asset is in a structural de-rating rather than a tactical dip. We would revisit if ETH reclaims $2,500 on a weekly close with positive funding.

Solana at $85.42 gained +1.4% WoW, a modest outperformance against the broader crypto complex, but remains -32.7% YTD. The intel block carries limited Hyperliquid-specific positioning data for SOL this week, which itself is informative: reduced derivatives activity in a mid-cap token during a risk-off regime typically signals low conviction from both bulls and bears. SOL's 52-week range of $77.86 to $247.47 places the current price in the lower quartile, and the neutral trend and OBOS readings confirm the absence of a directional catalyst. Without clear smart-money positioning data, we hold SOL at neutral and would require a break above $100 with rising open interest to consider an overweight stance.

XRP at $1.3484 fell -0.8% WoW and is -28.2% YTD, trading in the lower third of its 52-week range ($1.21-$3.09). The Hyperliquid aggregate data indicates XRP is part of the broad short positioning across majors, consistent with the risk-off theme. The neutral trend and OBOS readings offer no technical catalyst for a reversal. XRP's correlation with BTC remains high during sell-offs but its beta is amplified on the downside, making it a poor risk-adjusted hold in the current environment. We are neutral, with no conviction to take a directional view absent a regulatory or adoption catalyst.

BNB at $655.18 was the strongest major this week at +2.5% WoW, though it remains -24.1% YTD. The relative outperformance is modest and likely reflects exchange-specific flows rather than a fundamental re-rating. BNB's 52-week range of $582.91 to $1,306.60 places it in the lower half, and the neutral trend reading confirms range-bound trading. Without specific Hyperliquid cohort data for BNB in this week's intel, we lack the granularity to differentiate its positioning from the broad crypto short lean. We hold neutral, viewing BNB as a beta play on exchange volumes rather than a standalone allocation thesis.

What We're Watching

The 10Y yield at 4.67% is the week's critical threshold. A weekly close above that level would confirm the bond market is pricing a hike cycle, not a single adjustment, and we would shift SPY to UW and add to our duration short. On the downside, a sustained WTI close below $95/bbl would signal the Trump-Iran Hormuz deal is durable, collapsing the war premium and pulling the 10Y back toward 4.20-4.30%, at which point we would flip to neutral on duration. In equities, an S&P 500 weekly decline exceeding 3% from current levels ($723 or below on SPY) would indicate the rates repricing is finally transmitting to risk assets. In crypto, BTC reclaiming $85,000 with positive funding would challenge our neutral stance.

This Week in Charts